The Definitive Guide to Mortgage Investment Corporation

The Definitive Guide to Mortgage Investment Corporation

Blog Article

Mortgage Investment Corporation Can Be Fun For Anyone

Table of ContentsGetting The Mortgage Investment Corporation To WorkWhat Does Mortgage Investment Corporation Mean?Everything about Mortgage Investment CorporationMortgage Investment Corporation Can Be Fun For AnyoneGet This Report on Mortgage Investment Corporation

Does the MICs credit board review each home loan? In most scenarios, mortgage brokers take care of MICs. The broker must not work as a member of the credit scores board, as this puts him/her in a straight dispute of interest considered that brokers typically earn a payment for positioning the home loans. 3. Do the supervisors, participants of credit rating committee and fund manager have their own funds invested? Although an of course to this question does not provide a safe investment, it must supply some boosted safety and security if evaluated together with various other sensible loaning plans.Is the MIC levered? Some MICs are levered by a monetary organization like a legal bank. The banks will approve particular home mortgages had by the MIC as security for a credit line. The M (Mortgage Investment Corporation).I.C. will certainly after that obtain from their credit line and provide the funds at a greater price.

It is essential that an accounting professional conversant with MICs prepare these declarations. Thank you Mr. Shewan & Mr.

7 Easy Facts About Mortgage Investment Corporation Shown

This does not suggest there are not risks, however, normally speaking, no matter what the wider securities market is doing, the Canadian real estate market, especially major cities like Toronto, Vancouver, and Montreal carries out well. A MIC is a corporation formed under the policies lay out in the Earnings Tax Obligation Act, Area 130.1.

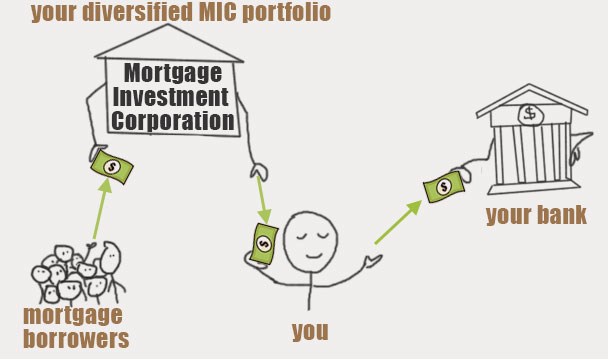

The MIC gains earnings from those home mortgages on rate of interest charges and basic charges. The genuine charm of a Home loan Financial Investment Firm is the return it offers capitalists contrasted to various other fixed revenue investments. You will have no problem discovering a GIC that pays 2% for a 1 year term, as federal government bonds are similarly as reduced.

The smart Trick of Mortgage Investment Corporation That Nobody is Discussing

A MIC needs to be a Canadian company and it need to spend its funds in mortgages. That said, there are times when the MIC ends up owning the mortgaged residential property due to repossession, sale arrangement, and so on.

A MIC will make rate of interest earnings from home loans and any type of cash the MIC has in the financial institution. As long as 100% of the profits/dividends are offered to investors, the MIC does not pay any kind of revenue tax obligation. Rather than the MIC paying tax on the passion it earns, shareholders are accountable for any tax obligation.

MICs issue common read more and recommended shares, issuing redeemable preferred shares to shareholders with a taken care of returns rate. For the most part, these shares websites are thought about to be "qualified financial investments" for deferred earnings plans. This is suitable for financiers who acquire Home mortgage Financial investment Company shares through a self-directed licensed retired life savings strategy (RRSP), signed up retirement income fund (RRIF), tax-free financial savings account (TFSA), delayed profit-sharing plan (DPSP), signed up education savings strategy (RESP), or registered impairment financial savings plan (RDSP).

And Deferred Plans do not pay any tax obligation on the rate of interest they are estimated to get. That said, those who hold TFSAs and annuitants of RRSPs or RRIFs may be struck with specific fine tax obligations if the investment in the MIC is taken into consideration to be a "restricted investment" according to Canada's tax code.

The Basic Principles Of Mortgage Investment Corporation

They will guarantee you have actually discovered a Home mortgage Investment Corporation with "competent financial investment" standing. If the MIC certifies, it might be really helpful come tax obligation time since the MIC does not pay tax obligation on the passion income and neither does the Deferred Plan. Mortgage Investment Corporation. Much more generally, if the MIC fails to satisfy the needs established out by the Revenue Tax Act, the MICs income will be exhausted prior to it gets distributed to shareholders, decreasing returns considerably

It appears both the realty and stock exchange in Canada go to all time highs At the same time returns on bonds and GICs are still near document lows. Also money is shedding its appeal due to the fact that energy and food prices have pushed the rising cost of living rate to a multi-year high. Which pleads the inquiry: Where can we still discover worth? Well I think I have the answer! In May I blogged regarding looking right into mortgage investment companies.

The Ultimate Guide To Mortgage Investment Corporation

If rate of interest rise, a MIC's return would likewise enhance since greater home mortgage prices suggest even more profit! People who invest in a mortgage financial investment corporation do not own the property. MIC investors merely earn money from the enviable setting of being a loan provider! It resembles peer to peer loaning in the united state, Estonia, or other components of Europe, except every finance in a MIC is protected by genuine residential property.

Many hard functioning Canadians who desire to get a home can not get home mortgages from standard banks because maybe they're self utilized, or don't have a well established credit report history. Or possibly they want a short-term car loan to create a huge property or make some restorations. Banks often tend to neglect these possible customers because self used Canadians don't have secure incomes.

Report this page